What Does Your Money Actually Cost You Every Month? How to Get That Number Right

The Question That Changes Everything

Here is a question I ask every single person who sits down with me — whether they are a longtime client, someone rebuilding after a rough stretch, or a professional woman getting serious about retirement.

What does it cost you to live every month?

You would be surprised how many people go quiet.

Not because they are embarrassed. But because they genuinely do not know.

And that is not a character flaw. That is just what happens when no one ever sat down and walked you through how to figure it out. Life gets busy. Money comes in, money goes out, and somehow we trust that it is all working — until it isn't.

I have been a financial advisor for over 30 years. I have worked with clients who have millions and clients who are starting over with almost nothing. And one thing holds true across the board: you cannot build a solid financial future on a number you're guessing at.

So today, let's fix that.

Why Most People Get This Wrong

The most common mistake people make when they try to figure out their monthly expenses is that they only think about the bills that show up every month.

Rent or mortgage? Yes. Car payment? Sure. Utilities? Probably.

But what about your car insurance that comes due twice a year? The annual subscription you forgot you had? The dentist visit you pay out of pocket every spring? The holiday travel you put on a card and pay off slowly?

Those expenses are real. They are part of your cost of living. They just do not arrive in a tidy monthly envelope.

The fix is simple: if something only comes around once or twice a year, divide it by 12 and count it as a monthly number. That way, your monthly picture is actually accurate — and you stop being blindsided by expenses you technically knew were coming.

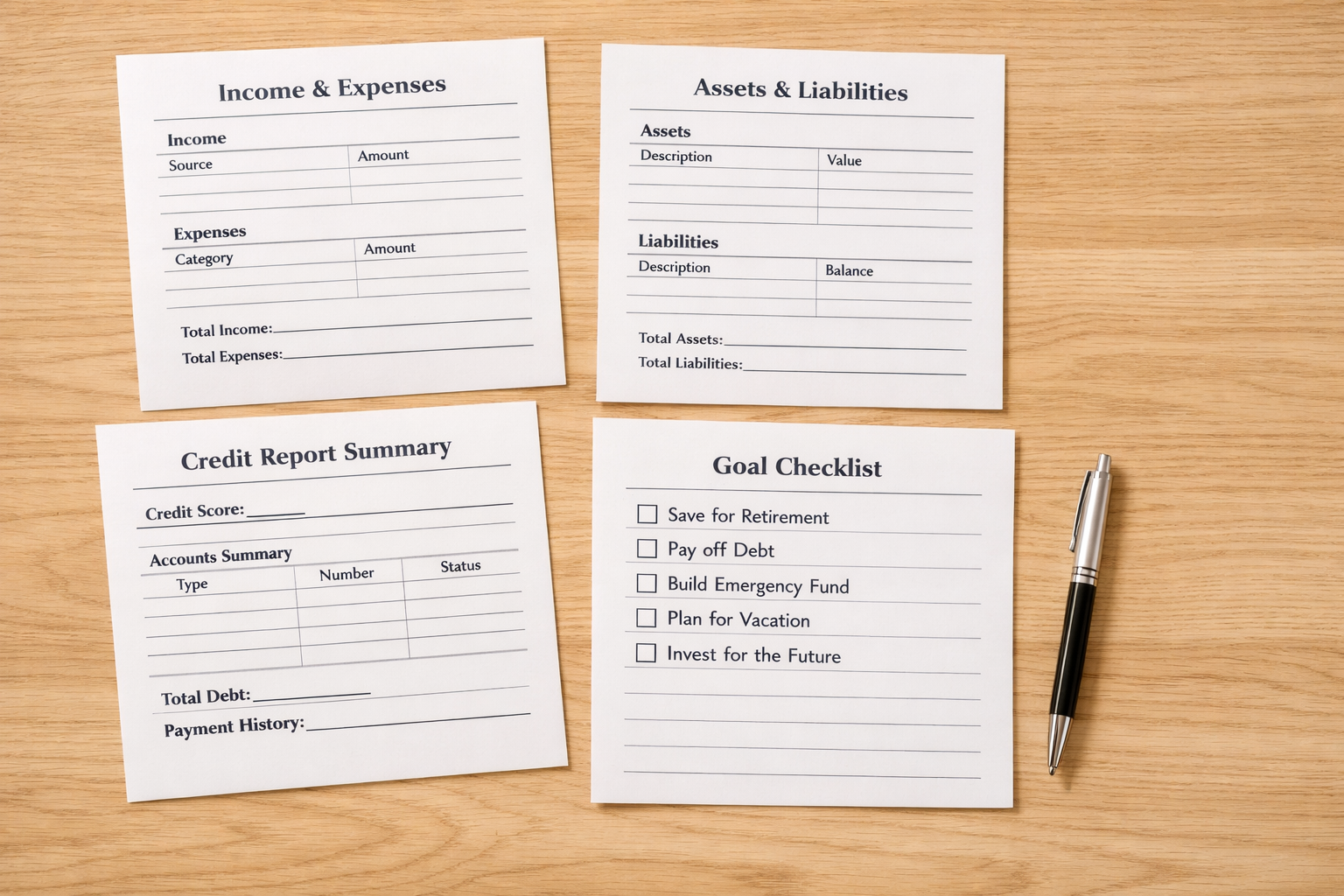

The 4 Worksheets That Give You the Full icture

Over the years, I have refined a process I use with every new client. It starts with four worksheets. I give them out at the first meeting and ask people to fill them in before we talk. You can do this yourself, too.

Worksheet 1: Income and Expenses

Write down everything coming in and everything going out. List every expense, then go back and look for the ones that only hit once or twice a year. Divide those out to a monthly number and add them to your list. At the end, you want one honest number: what does it actually cost you to live each month?

Worksheet 2: Assets and Liabilities

What do you own, and what do you owe? List your assets — savings, investments, property, retirement accounts. Then list your debts — and next to each one, write down the interest rate. That interest rate column matters more than most people realize. We will come back to that.

Worksheet 3: Your Credit Report

You can pull all three credit agency reports for free once a year. Do it. Look at your score, and look at what is on there. There may be accounts you forgot about, old debts still affecting your score, or errors that are costing you money every single day. Your credit score affects more than just loans — it can influence your car insurance, your home insurance, even whether you get a job offer. It is worth knowing.

Worksheet 4: Your Goals and Concerns

This one is different. I ask people three things: What concerns you most about your financial future? What are your goals? And do you feel like your income is currently covering your monthly expenses?

I will be honest with you — the goal answers I get back are often things like, "I want to live comfortably." And as much as I appreciate the sentiment, that is not a goal. That is a wish.

A goal has a number attached to it. It has a timeline. "I want to travel to Italy at 67 and have $15,000 set aside for the trip." That is something we can work with.

From Wishful Thinking to a Real Plan

Once you have those four worksheets filled in honestly, something interesting happens. You stop feeling like money is this vague, unpredictable force in your life. You start seeing it as a system — one you can actually manage.

The second part of the process is a conversation. We look at the goals together and get specific. We ask the questions that turn a wish into a target. And then — this is the part that surprises people — we stop trying to control outcomes and start talking about actions.

We cannot control the market. We cannot control inflation. We cannot control what happens to Social Security. But we can control what we do consistently, week after week, that moves us in the direction we want to go.

That shift in thinking — from "I hope things work out" to "here is what I am doing about it" — is where real financial confidence starts.

A Real Example (With the Names Left Out)

I do pro bono financial counseling on the side, working with people who are rebuilding their lives after some genuinely hard circumstances. One of the biggest battles I have with these folks is getting them to accurately account for their monthly expenses.

One person handed me a budget that had no food listed. No childcare. I looked at them and said, "You have children who are not in school yet. How is childcare not on here?"

I was not being harsh. I was being honest — because without that number, nothing else I could tell them would help. The plan has to be built on reality, not the version of reality we wish we were living.

The same thing happens with more established clients. I had a client who kept making large withdrawals from a retirement account — tens of thousands of dollars at a time — while also taking on a car payment she couldn't comfortably afford on her income. When we sat down and looked at the actual numbers together, the picture was pretty stark.

That is not a judgment. That is what happens when the real monthly cost of living goes unexamined for too long.

Where to Start If This Feels Overwhelming

If you read all of this and your immediate reaction is, I don't even know where to begin, let me make it simple.

Start with one question: What is coming in every month, and what is going out?

You do not need a fancy app (though there are decent ones out there). You do not need a spreadsheet with color coding. You need a piece of paper, a pen, and a commitment to be honest with yourself.

If the number you get at the end surprises you — if your income and your expenses do not match the way you thought they did — that is actually good information. It means you now know something you didn't know before. And now you can do something about it.

Ready to Build Your Blueprint?

If you are a professional woman thinking seriously about what retirement looks like for you, this kind of honest financial foundation is where everything starts.

I have a free ebook — Build Your Future Blueprint — that walks you through the first steps of getting your financial picture clear so you can start planning with confidence.

Or if you would rather just talk through where you are and what you're trying to accomplish, I offer a complimentary 30-minute get acquainted call. No pressure. Just an honest conversation.

You have worked too hard to leave your financial future to chance. Let's get the real numbers on paper — and go from there.